Are you a small business owner wondering about your tax obligations? You might be asking yourself, “Can I file my small business taxes separately from my personal taxes?”

This question is crucial for maintaining your financial health and ensuring compliance with tax laws. Understanding the nuances of business and personal tax filings can save you money and reduce stress. We’ll break down the key points you need to know about filing your taxes, the benefits of separating your business and personal finances, and how to navigate this important process.

Keep reading to find out how you can simplify your tax season and make the most of your hard-earned income.

Small Business Vs. Personal Taxes

Understanding the difference between small business taxes and personal taxes is crucial for any entrepreneur. It can impact your financial health and business decisions. Let’s break it down.

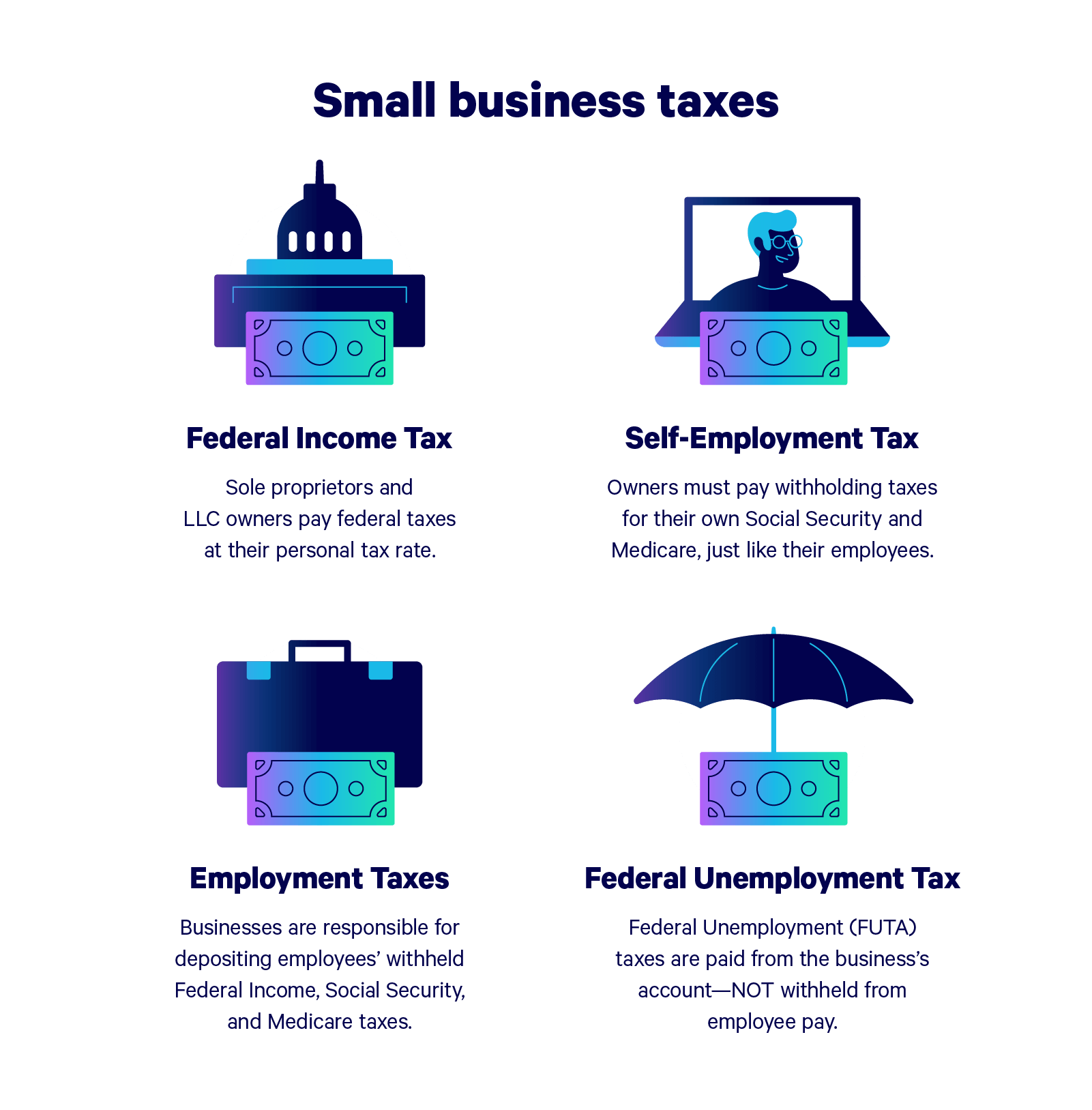

What Are Small Business Taxes?

Small business taxes refer to the taxes that a business owner must pay based on their business income. This includes federal, state, and local taxes. Different business structures, such as sole proprietorships, partnerships, or corporations, have various tax obligations.

- Self-Employment Tax:This tax applies to income earned from your business. It covers Social Security and Medicare.

- Income Tax:Depending on your business structure, profits may be taxed at individual rates or corporate rates.

- Sales Tax:If you sell goods or services, you may need to collect and remit sales tax.

What Are Personal Taxes?

Personal taxes are taxes you pay on your individual income. This includes wages from employment, rental income, and any other personal earnings. These taxes also cover personal deductions and credits that can affect how much you owe.

- Federal Income Tax:Based on your income level, you pay a certain percentage to the federal government.

- State Income Tax:Many states impose their own income tax, which varies by state.

- Property Tax:If you own property, you’ll pay property taxes to your local government.

Can You File Separately?

Yes, you can file small business taxes separately from personal taxes, but it depends on your business structure. For instance, a sole proprietor typically reports business income on their personal tax return using Schedule C. In contrast, a corporation files its own tax return.

Consider the advantages of separating your taxes. It can simplify your financial reporting and clarify your business’s profitability. However, it may also require more paperwork.

Why Does It Matter?

Understanding these differences is vital for your financial planning. It influences your tax liabilities and potential deductions. You want to maximize your savings and minimize your stress during tax season.

Have you thought about how your business structure affects your tax responsibilities? Keeping your personal and business finances separate can lead to better organization and more accurate financial insights. You want to ensure you’re not leaving money on the table come tax time.

:max_bytes(150000):strip_icc()/business-entities-3193420_final-9806a9e0701a4f60b9e06d36e0e0338b.png)

Credit: www.thebalancemoney.com

Tax Structures For Small Businesses

Small business owners often wonder about tax filing. Can you file small business taxes separately from personal taxes? Yes, it is possible, depending on your business structure. Different structures have different rules, which can affect how you file your taxes.

When starting a small business, understanding your tax structure is vital. It can affect how you file your taxes and whether you can separate your personal finances from your business. Each tax structure comes with its own rules, benefits, and drawbacks. Let’s break down the main types of tax structures for small businesses.Sole Proprietorships

A sole proprietorship is the simplest business structure. It’s easy to set up and requires minimal paperwork. However, this means your business income is reported on your personal tax return. You might find that all profits and losses flow directly to your personal taxes. This can be a double-edged sword. While it simplifies tax filing, it also means your personal assets could be at risk if your business faces financial trouble.Partnerships

Partnerships involve two or more people sharing the business responsibilities. Like sole proprietorships, the income is passed through to your personal tax returns. Each partner reports their share of the profits or losses. This structure offers flexibility in terms of management and profit-sharing. However, you also share liability with your partners. If one partner faces issues, it can affect everyone involved.Llcs

Limited Liability Companies (LLCs) provide a mix of flexibility and protection. An LLC can protect your personal assets from business liabilities. This means if your business faces a lawsuit, your personal savings and property are generally safe. You can choose how your LLC is taxed—either as a sole proprietorship or a corporation. This flexibility allows you to maximize your tax benefits. You can still file your taxes separately from your personal income, depending on how you set it up.Corporations

Corporations are more complex and require more paperwork. They are separate legal entities, meaning your personal assets are generally protected from business liabilities. Corporations can also offer benefits like stock options and employee benefits. However, they face double taxation—once at the corporate level and again on dividends paid to shareholders. This can be a downside if you’re looking to maximize your earnings. Choosing the right tax structure is crucial for your business. What structure feels right for you? Consider your financial situation, risk tolerance, and long-term goals. This will set the stage for your business’s financial health.Filing Separately Vs. Filing Together

Filing small business taxes separately from personal taxes is possible. This choice can affect your tax rates and deductions. Understanding the differences helps in making the right decision for your financial situation.

Understanding whether to file small business taxes separately from personal taxes is crucial for every entrepreneur. This choice affects your financial situation and future planning. Let’s break down what this means for you by looking at the differences between filing separately and filing together.How Sole Proprietors Report Taxes

Sole proprietors report their business income on Schedule C, which is attached to their personal tax return (Form 1040). This means all profits and losses from your business flow directly to your personal tax return. You’ll pay self-employment taxes on your net earnings as well. This can feel overwhelming, especially if your business isn’t generating consistent income. Keeping accurate records of your expenses can help you lower your taxable income. Consider your unique situation. Do you have significant business expenses that might offset your income? If yes, filing together may offer some advantages.When Separation Is Required

Certain situations require you to file separately. If your business is structured as a corporation or a partnership, you cannot combine your personal and business taxes. Also, if you’re in a business that has potential liability issues, keeping your finances separate can protect your personal assets. This is especially true for real estate businesses or those involving high-risk activities. If you find yourself in a complex tax situation, consulting with a tax professional is wise. They can guide you on the best filing method tailored to your needs.Benefits Of Filing Separately

Filing separately can offer several advantages. For one, it can simplify your financial management. Keeping business and personal finances distinct helps with clarity and organization. Additionally, you may qualify for specific deductions or credits that aren’t available if you file jointly. This can lead to potential savings. You might also want to consider the implications for your personal finances. Are you carrying significant debt or liabilities? Separating your taxes can help shield your personal assets from your business risks. Take a moment to think about your long-term goals. How do you want your business to grow? Your choice of tax filing can influence your financial trajectory significantly.Business Entity And Tax Filing Requirements

Understanding how to file small business taxes is important. The rules can change based on your business type. Each business entity has different tax filing needs. Knowing these can help you save money and avoid issues.

Pass-through Entities And Personal Taxes

Pass-through entities include sole proprietorships, partnerships, and LLCs. These businesses do not pay taxes at the business level. Instead, profits pass through to the owners. Owners report this income on their personal tax returns.

This means your business profits are taxed at your individual tax rate. It simplifies the process for many small business owners. Tracking income and expenses is still crucial. Accurate records help ensure correct tax reporting.

Corporations And Separate Tax Returns

Corporations, unlike pass-through entities, file separate tax returns. They pay corporate taxes on their profits. This can lead to double taxation if dividends are paid to shareholders. Shareholders then pay taxes on their personal returns.

Choosing to form a corporation may offer benefits. It provides liability protection and may lower self-employment taxes. However, the tax filing process is more complex. Consult a tax professional to understand your options.

Deductions And Expenses For Small Businesses

Deductions and expenses play a crucial role in managing your small business taxes effectively. Understanding what you can deduct not only reduces your taxable income but also helps you keep more of your hard-earned money. Let’s dive into the specifics of common deductions and the importance of recordkeeping.

Common Business Deductions

Identifying the right deductions can significantly lower your tax bill. Here are some common business deductions you might be eligible for:

- Office Supplies:Items like paper, pens, and other supplies used in your business can be deducted.

- Home Office:If you work from home, you can deduct a portion of your rent or mortgage interest, utilities, and internet expenses.

- Travel Expenses:Costs related to business travel, including airfare, hotel stays, and meals, are deductible.

- Vehicle Expenses:If you use your vehicle for business, you can deduct either the actual expenses or use the standard mileage rate.

- Marketing Costs:Expenses for advertising and promotions can also be deducted.

Think about your own business. Have you been capturing all the eligible expenses? It’s easy to overlook costs that can add up to significant savings.

Recordkeeping For Tax Accuracy

Accurate recordkeeping is vital for claiming deductions and avoiding issues with the IRS. Make it a habit to keep all receipts and invoices related to your business expenses. Organizing them can save you time and stress during tax season.

Consider using accounting software or apps to track your expenses. These tools can simplify the process and ensure you don’t miss any deductions. – Create separate accounts for business and personal expenses. – Regularly update your records to avoid last-minute scrambles.

Have you ever had difficulty recalling your expenses come tax time? Keeping meticulous records can eliminate that worry and help you maximize your deductions.

Credit: www.johansonllp.com

Choosing The Right Tax Filing Option

Choosing the right tax filing option for your small business is crucial. It can have a significant impact on your finances and stress levels. Understanding your choices will help you make informed decisions and optimize your tax situation.

Consulting A Tax Professional

Working with a tax professional can simplify the tax filing process. They can guide you through the complexities of small business taxes and help you identify deductions you might miss. A tax pro will also stay updated on changes in tax law, ensuring you remain compliant.

Think about your situation. Do you have multiple income streams or complicated expenses? A tax professional can offer personalized advice tailored to your unique needs.

Factors To Consider

Several factors influence your tax filing option. Consider your business structure first. If you operate as a sole proprietor, your business income will typically be reported on your personal tax return.

- Business Structure:Your entity type (LLC, corporation, etc.) determines how you file.

- Income Level:Higher income may prompt different filing strategies.

- Deductions:What expenses can you claim? Knowing this helps maximize your returns.

Your time and resources also matter. Are you comfortable managing your taxes, or would you prefer to outsource? Assessing your skills and availability can guide your choice.

Have you considered the long-term implications of your filing choice? A decision made today can affect your future tax responsibilities. Make sure to weigh all options carefully.

Common Mistakes To Avoid

Filing small business taxes can be tricky. Many business owners make mistakes. These errors can lead to penalties or missed deductions. Avoiding common mistakes is essential for smooth tax filing.

Mixing Business And Personal Finances

One big mistake is mixing business and personal finances. Keep separate bank accounts for business and personal use. This helps track income and expenses clearly. Mixing them can complicate your tax filings.

Using personal funds for business expenses? This can lead to confusion. Always use your business account for business purchases. This makes it easier to prove expenses when filing taxes.

Overlooking Required Tax Forms

Another common mistake is overlooking required tax forms. Many small business owners miss deadlines for important forms. Familiarize yourself with all necessary tax documents.

Forms like Schedule C, Form 1099, and others may apply. Ensure you know what you need to file. Missing forms can lead to fines and delays in processing.

Credit: www.embroker.com

Frequently Asked Questions

Can I File Small Business Taxes Separately?

Yes, you can file small business taxes separately from your personal taxes. This is common for sole proprietors, LLCs, and corporations. Separate filings help clarify your business income and expenses. It also simplifies the tax reporting process, ensuring accuracy and compliance with IRS regulations.

What Are The Benefits Of Separate Tax Filings?

Filing small business taxes separately offers several benefits. It helps maintain clear records for business income and expenses. Separate filings can also maximize deductions and credits. This approach minimizes the risk of personal liability and provides a clearer financial picture for potential investors or lenders.

What Forms Do I Need For Separate Filings?

For separate filings, you’ll typically use specific IRS forms. Sole proprietors generally file a Schedule C along with their 1040 form. Corporations file Form 1120, while partnerships use Form 1065. Make sure to keep accurate records for all business-related income and expenses to support your filings.

Can I Deduct Personal Expenses On Business Taxes?

No, personal expenses cannot be deducted on business taxes. Business expenses must be ordinary and necessary for your trade or business. Mixing personal and business expenses can lead to tax complications and potential penalties. Always maintain clear separation between personal and business finances for accurate reporting.

Conclusion

Filing small business taxes separately from personal taxes is possible. This choice depends on your business structure. Sole proprietors often report income on personal returns. Corporations and LLCs have different rules. Consult a tax professional for guidance. They can help you understand your options.

Keeping these taxes separate can simplify your finances. It may also protect your personal assets. Take time to learn about your tax responsibilities. This knowledge will benefit you and your business in the long run.