Starting a small business is a thrilling adventure, filled with dreams and ambitions. But have you ever wondered how many small businesses fail in the first year?

It’s a shocking reality that many aspiring entrepreneurs face. You might be excited to launch your own venture, but understanding the risks is crucial for your success. Knowing the statistics can help you prepare and avoid common pitfalls. We’ll explore the hard facts behind small business failures and share insights that could change your approach.

By the end, you’ll be equipped with the knowledge to increase your chances of thriving in your first year and beyond. Don’t let your dreams fade—let’s dive in!

Small Business Survival Rates

Understanding small business survival rates is crucial for any entrepreneur. Many new businesses face significant challenges in their first year. The statistics can be startling, but they also provide valuable insights into what it takes to succeed.

What Are The Survival Rates?

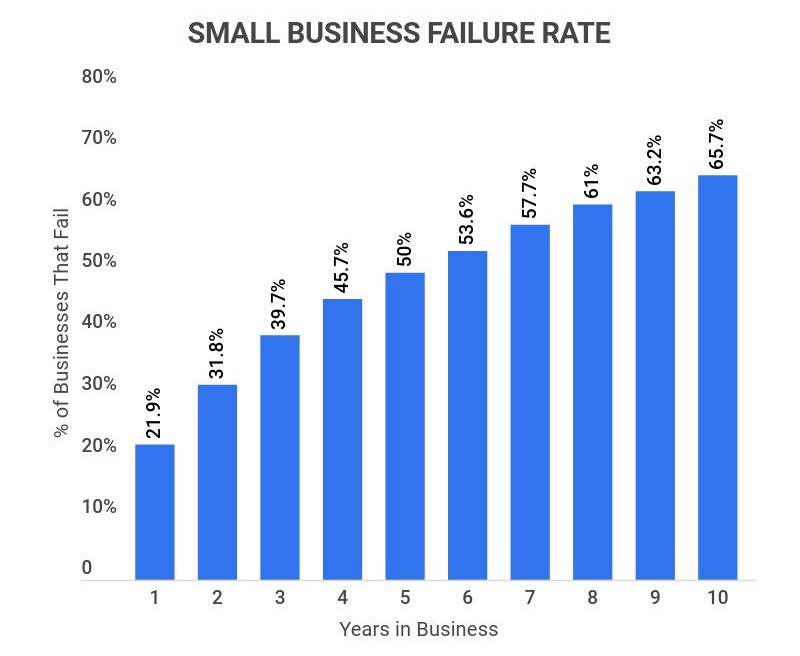

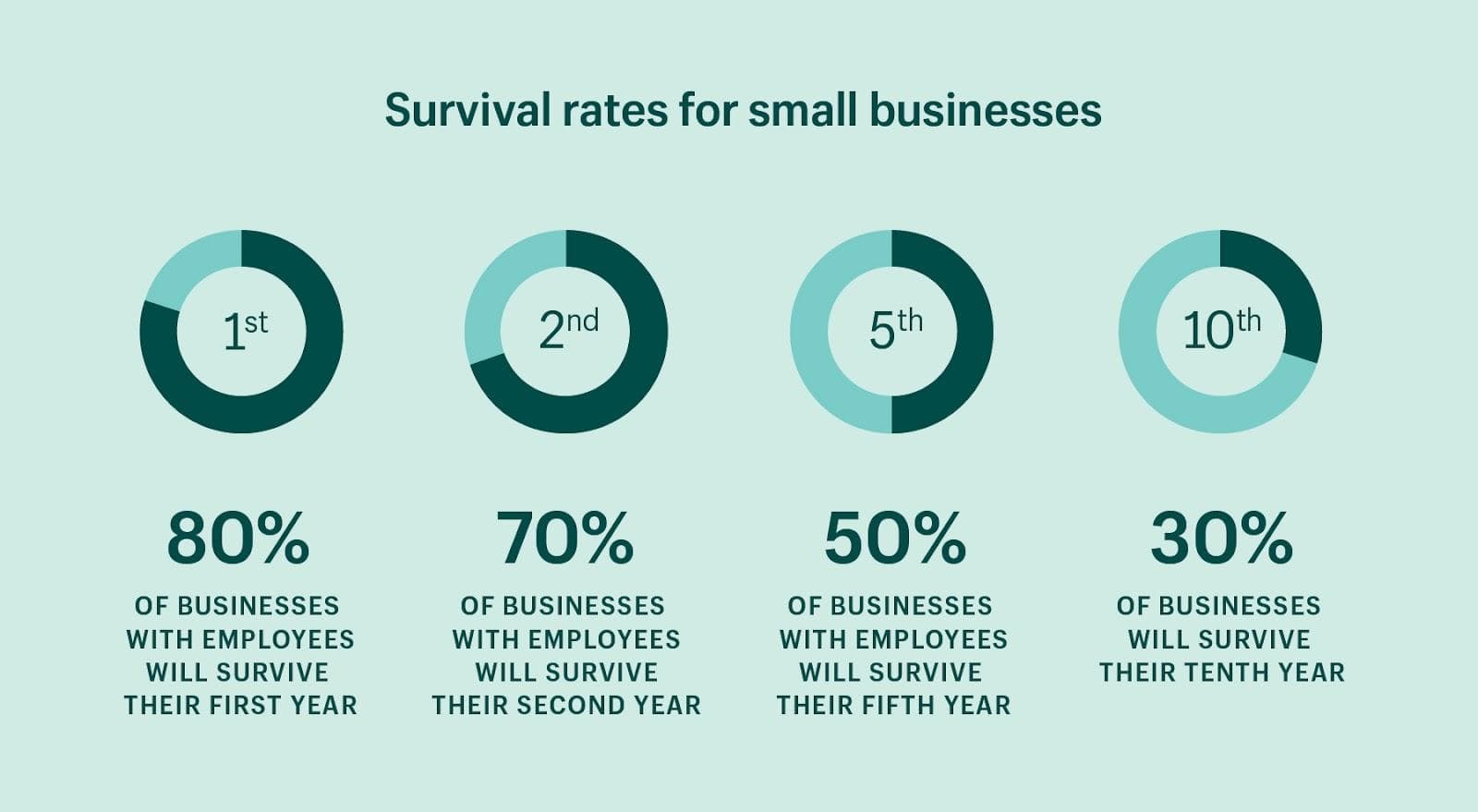

Statistics show that about 20% of small businesses fail within their first year. This means that only 80% make it past that critical milestone. It’s essential to consider what factors contribute to these numbers.

- Lack of Market Demand:Many businesses launch without sufficient research into what customers actually want.

- Poor Financial Management:Mismanaging cash flow can quickly lead to bankruptcy.

- Inadequate Planning:Failing to create a solid business plan often leads to missed opportunities.

These reasons highlight the importance of thorough preparation before starting your business. Have you taken the time to evaluate your market and financial plans?

The Importance Of Adaptability

Small businesses that adapt to changing market conditions tend to survive longer. Flexibility allows you to pivot when necessary. If your initial idea isn’t working, can you change your approach?

When I started my first business, I quickly learned that my initial product didn’t resonate with customers. Instead of giving up, I asked for feedback and adjusted my offerings. This change not only saved my business but also led to better sales.

Building A Strong Support System

Networking can play a vital role in survival rates. Connecting with other business owners can provide support and advice. Have you reached out to your local business community?

Consider attending local meetups or joining online forums. These connections can help you navigate challenges and share resources that can lead to success.

Taking Calculated Risks

Every business decision involves some level of risk. However, taking calculated risks can lead to significant rewards. Are you willing to step out of your comfort zone to achieve your goals?

Successful entrepreneurs often share stories of risks they took that paid off. Carefully evaluate your options and don’t shy away from making bold moves when the situation calls for it.

Knowing the survival rates and common pitfalls can empower you. Your journey as a small business owner may be challenging, but with the right strategies, you can increase your chances of success. What steps will you take today to ensure your business thrives?

Credit: www.zippia.com

Common Reasons For Failure

Many small businesses struggle in their first year. Understanding why can help new owners succeed. Here are some common reasons for failure.

Lack Of Market Demand

One major reason small businesses fail is lack of market demand. Some owners do not research their target audience. They may offer products or services that few people want. Without customers, sales drop. This leads to financial problems.

Poor Financial Management

Another critical issue is poor financial management. Many small business owners lack experience in budgeting. They might overspend on unnecessary items. Keeping track of expenses is essential. Without proper management, businesses can run out of cash quickly.

Ineffective Marketing Strategies

Ineffective marketing strategies can also hurt a business. Some owners do not know how to reach their audience. They may spend money on ads that do not work. Good marketing is vital for attracting customers. Without it, sales will suffer.

Operational Challenges

Operational challenges can create many problems for small businesses. Managing staff, inventory, and supply chains can be tough. Poor organization leads to inefficiency. This can frustrate customers and reduce sales. Streamlining operations is crucial for success.

Industries With Higher Failure Rates

Many small businesses struggle in their first year. Statistics show that about 20% fail within this time. Certain industries, like restaurants and retail, face even higher failure rates, making it crucial for new owners to plan carefully.

Understanding which industries face higher failure rates can help you make informed decisions if you’re considering starting a small business. Some sectors are notoriously tough, with many new ventures closing their doors within the first year. Let’s break down the industries that struggle the most.Food And Beverage

The food and beverage industry is one of the hardest sectors for new businesses. High competition, changing consumer tastes, and tight margins play a significant role in the struggles faced by new restaurants and cafes. Many entrepreneurs enter this space with passion but overlook crucial factors like location, staffing, and inventory management. A personal experience comes to mind—my friend opened a trendy café, but within six months, they faced challenges due to high rent and fluctuating food prices. Did you know that nearly 60% of restaurants fail within their first year? This stat highlights the importance of thorough market research and a solid business plan.Retail

Retail businesses also have a high failure rate, particularly brick-and-mortar stores. The rise of e-commerce has shifted consumer shopping habits dramatically. Imagine investing your savings into a boutique, only to find that most of your potential customers prefer shopping online. This is the reality many new retailers face. Additionally, factors like inventory issues and seasonal sales can be detrimental. According to reports, about 30% of new retail businesses close within their first year. You need a strong online presence and a unique selling proposition to stand out. Have you thought about how your retail business can adapt to this changing landscape?Technology Startups

Technology startups are often viewed as the future, but they also face significant hurdles. Rapidly evolving technology and market demands can lead to quick failures. Many startups spend too much time perfecting their product without validating their market need. A friend of mine launched a tech app that seemed brilliant, but after a year, it flopped due to a lack of user interest. Statistics show that about 20% of tech startups fail within their first year. To increase your chances of success, prioritize market research and customer feedback. What steps are you taking to ensure your tech venture meets the needs of your target audience? Understanding these industries’ challenges can help you navigate the rocky path of entrepreneurship. Knowledge is your best ally in turning your business dreams into reality.

Credit: www.facebook.com

The Role Of Location And Demographics

The success of a small business often hinges on its location and the demographics of its target audience. The right spot can draw in customers, while the wrong one can lead to failure. Understanding these factors can significantly impact your bottom line.

The Impact Of Location On Business Success

Your business location can either make or break your venture. A bustling area with high foot traffic can increase visibility and sales. Conversely, a remote or low-traffic spot can stifle growth.

Consider a coffee shop positioned near a university. Students flock to nearby cafes for a quick study break or socializing. This location takes advantage of the student demographic, driving steady sales.

Another aspect to consider is competition. A location with many similar businesses can be a double-edged sword. While it may indicate a strong market, it can also saturate the customer base.

Understanding Your Demographics

Knowing your target audience is crucial. Different demographics have distinct preferences, buying habits, and income levels. Tailoring your business to meet these needs can enhance your chances of success.

- Age:Younger customers might prefer trendy products, while older customers may seek quality and service.

- Income:Higher-income areas might support premium pricing, whereas lower-income areas may require budget-friendly options.

- Cultural Factors:Local culture can influence product demand, from food preferences to fashion trends.

Have you ever wondered why certain businesses thrive in specific neighborhoods? It’s all about understanding who your customers are and what they want.

Adapting To Local Trends

Staying attuned to local trends can set you apart from competitors. If your area embraces sustainability, offering eco-friendly products could attract attention. Similarly, if a community values local artisans, stocking handmade items might resonate well.

Engaging with your community can provide insights into local preferences. Attend local events or engage on social media to learn what your audience values. This approach not only informs your business strategy but also fosters loyalty.

<pYour location and understanding of demographics are pivotal. They can guide your decisions and help you connect with your audience. How well do you know the market where you operate?Impact Of Economic Factors

Many small businesses face challenges in their first year. Economic factors play a big role. Understanding these factors helps explain why many fail.

Market conditions change quickly. These changes can make it hard for new businesses to survive. Let’s explore two major economic factors: recessions and access to capital.

Recession And Slowdowns

A recession can hit small businesses hard. During a recession, people spend less money. They cut back on non-essential items. This drop in spending affects sales.

Small businesses often rely on steady customers. A slowdown can lead to fewer customers. This can result in lower revenue and higher risks of failure.

Access To Capital

Access to capital is crucial for small businesses. New businesses often need loans to start. Without proper funding, they struggle to grow.

During economic downturns, banks tighten lending. They become cautious with loans. This makes it harder for small businesses to get the money they need.

Lack of funds can limit growth and operations. Many small businesses fail because they cannot secure funding. Understanding these financial barriers is key for new entrepreneurs.

Lessons From Successful Businesses

Understanding the lessons from successful businesses can be your blueprint for navigating the challenging landscape of entrepreneurship. Many small businesses struggle, but those that thrive often share common traits. Let’s look at specific strategies that can set your business apart from the rest.

Strategic Planning

Successful businesses start with a solid plan. They know their goals and outline a clear path to achieve them.

- Define your mission:What purpose does your business serve? A strong mission statement keeps you focused.

- Set measurable goals:Use the SMART criteria—Specific, Measurable, Achievable, Relevant, Time-bound—to gauge your progress.

- Regular reviews:Check your plan against real-world performance. Adjust as needed to stay on course.

Consider a friend who launched a local coffee shop. They mapped out their target audience, marketing strategies, and financial projections. Regularly revisiting their plan allowed them to pivot quickly when trends changed, ultimately driving growth.

Customer-centric Approach

Putting customers at the center of your strategy is key. Successful businesses listen to their customers and adapt accordingly.

- Gather feedback:Use surveys or social media to learn what your customers want.

- Build relationships:Engaging with your customers creates loyalty. Respond to their needs and concerns promptly.

- Personalize experiences:Tailor your offerings to meet the unique preferences of your audience.

Your customers are your best asset. A local boutique owner I know often asks her customers for input on new products. This has not only increased sales but also strengthened her community ties.

Adaptability And Innovation

Businesses that adapt to changing circumstances thrive. The ability to innovate keeps you relevant.

- Stay informed:Keep an eye on industry trends and competitor strategies.

- Encourage creativity:Foster an environment where new ideas are welcomed and explored.

- Test and learn:Implement new strategies on a small scale first. Analyze results before a full rollout.

A tech startup I once consulted for had to pivot during the pandemic. They shifted from in-person services to online workshops. This adaptability not only saved them but also opened new revenue streams.

What strategies can you implement today to ensure your business not only survives but thrives? Consider your approach to planning, customer engagement, and adaptability. Learning from those who have succeeded can pave your way to success.

How To Improve Survival Odds

Improving the odds of survival for your small business is essential in today’s competitive landscape. Many entrepreneurs dive into their ventures with passion, but neglect the basics that can lead to failure. Understanding key strategies can significantly enhance your chances of success.

Building A Solid Business Plan

A well-thought-out business plan is your roadmap to success. It outlines your goals, strategies, and the steps you need to take to achieve them. Without a clear plan, you may find yourself lost or overwhelmed.

- Define your target market.

- Identify your competition.

- Set realistic financial projections.

Remember, a business plan isn’t static. Update it regularly to reflect changes in your market or business direction. Regular reviews will help you stay focused and adapt to new challenges.

Monitoring Cash Flow

Cash flow is the lifeblood of your business. Without it, even the best ideas can falter. Keep a close eye on your income and expenses to avoid unexpected surprises.

- Maintain a detailed cash flow statement.

- Track your daily, weekly, and monthly expenses.

- Set aside a buffer for emergencies.

Consider using accounting software to simplify this process. Having a clear understanding of your financial health allows you to make informed decisions and avoid cash shortages.

Seeking Expert Advice

Don’t hesitate to seek help from those who have been in your shoes. Consulting with industry experts or hiring a business coach can provide valuable insights. Their experience can help you navigate challenges and avoid common pitfalls.

Networking is also crucial. Attend workshops and join local business groups to connect with others who can offer support and advice. Sharing experiences can lead to new ideas and opportunities.

What steps will you take today to ensure your business thrives? Reflect on these strategies and consider how they can be tailored to your unique situation.

Credit: www.commerceinstitute.com

Frequently Asked Questions

What Percentage Of Small Businesses Fail In The First Year?

Approximately 20% of small businesses fail within their first year. This statistic highlights the challenges new entrepreneurs face. Factors like inadequate planning, lack of capital, and market competition contribute to these failures. Understanding these risks can help future business owners prepare better and improve their chances of success.

Why Do Small Businesses Struggle In The First Year?

Small businesses often struggle due to several key factors. Insufficient funding, poor market research, and lack of experience can hinder success. Additionally, unexpected expenses and economic fluctuations may impact operations. Awareness of these challenges can help entrepreneurs create effective strategies to navigate their first year.

How Can Small Businesses Succeed In The First Year?

To succeed in the first year, small businesses should focus on thorough planning. Creating a solid business plan helps outline goals and strategies. Additionally, securing adequate funding is crucial for operations. Building a strong network and adapting to market changes also contribute significantly to long-term success.

What Industries Have The Highest Failure Rates?

Industries with the highest failure rates include restaurants, retail, and construction. These sectors face intense competition and fluctuating consumer demand. Businesses in these areas often struggle with cash flow and operational challenges. Entrepreneurs should carefully evaluate market conditions before entering these high-risk industries.

Conclusion

Many small businesses face tough challenges in their first year. High failure rates show the need for careful planning. Understanding common pitfalls can help new owners succeed. Support, research, and good management make a big difference. Learning from others’ mistakes can save time and money.

Each step taken toward improvement counts. By staying informed and adaptable, small businesses can thrive. Success is possible with the right approach and dedication. Keep pushing forward, and don’t give up easily. Your business can become one of the success stories.